What Ontario’s New Housing Tax and Development Charge Changes Actually Mean

There’s been a lot of buzz around Ontario’s latest housing announcements. Big numbers. Big headlines. Plenty of people cheering or complaining before really knowing what was announced.

Fair enough. Most of this stuff is not explained well, and the headlines don’t help.

So here’s the plain-English version.

The federal government and Ontario have rolled out a group of measures meant to lower the cost of building and buying new-build housing. The idea is simple enough: if it costs less to build, maybe more homes get built, and maybe affordability improves.

That sounds good on paper, but the real questions are these:

Where is the money coming from?

Will buyers actually save money?

Will this really help affordability?

And are governments trying to flood the market with supply?

Let’s break it down.

What was actually announced?

There are two main pieces here.

1. The $8.8 billion infrastructure and development charge plan

On March 30, 2026, the federal government announced that it and Ontario will cost-match a total of $8.8 billion over 10 years for housing-enabling infrastructure. The funding is meant to support municipalities that reduce development charges by up to 50 percent for a three-year period, targeting areas that cover 80 percent of Ontario’s population.

That matters because development charges are one of the biggest costs builders face when putting up new housing.

The money is meant to go to municipalities that actually step up and reduce those charges. Vaughan is already at the front of the line, having cut development charges by 50 percent. Mississauga has done the same. Burlington has been talking about a two-year waiver, and Niagara is in the conversation as well.

Hopefully the money does get where it needs to go.

2. Ontario’s expanded HST rebate on new homes

This part is not just a proposal anymore. It is available now.

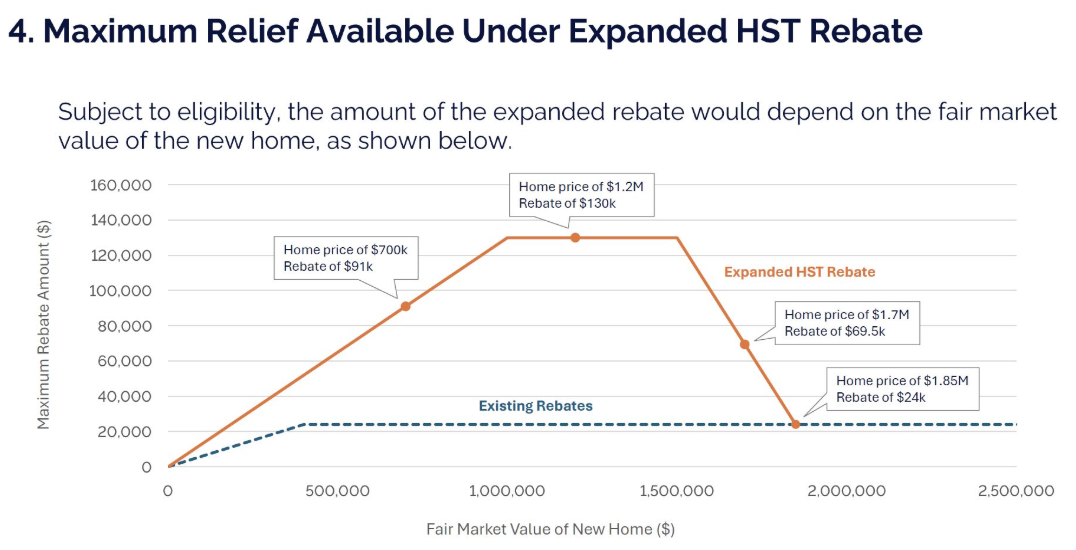

Ontario’s expanded HST rebate for new homes is in effect for agreements signed on or after April 1, 2026. This temporary measure removes the 8 percent provincial portion of HST on eligible new homes up to $1.5 million for one year, running until March 31, 2027, where the home is intended as a primary residence.

The other big change here is the price range. This is long overdue. The old rebate thresholds were built for a different market and became more and more disconnected from reality as prices climbed. Ontario has now moved the rebate into a range that actually reflects what new homes cost in a lot of markets today.

The relief also scales in a way that should get people’s attention. Around a $700,000 purchase price, the rebate is roughly $91,000. Around $1.2 million, it peaks at about $130,000, then begins tapering down toward $1.5 million.

Maximum Benefit: Full 13% HST rebate (up to $130,000) applies to homes up to $1.5 million.

Threshold Breakdown:

Up to $1 million: Full 13% rebate available.

$1M – $1.5 million: Maximum $130,000 rebate maintained.

$1.5M – $1.85 million: Rebate decreases proportionally from $130,000 to $24,000.

Over $1.85 million: The rebate drops to the existing pre-2026 maximum of $24,000.

What are development charges?

Development charges are fees municipalities charge on new development to help pay for growth-related infrastructure.

Think roads, water, wastewater, and other services needed when a community gets bigger.

So when builders say these fees matter, they’re right. They are part of the total cost of building. And when those costs go up, the final price of the home goes up too. Builders do not just absorb that cost out of the goodness of their hearts. It gets passed along to you.

Does cutting development charges automatically make housing cheaper?

No. Not automatically.

This is where people need to slow down.

If you lower one cost for a builder, that helps. But it does not guarantee that buyers will see the full savings.

A lower development charge improves the math on a project. That can make more projects viable. It can help some projects move forward that otherwise would not. That part is real. We’ve seen this already in some municipalities.

Vaughan has already pulled the trigger. Neighbouring Markham however, refuses to cut the charges citing a $458 Million shortfall in revenue over five years. This revenue would need to be made up which can only mean one thing, a projected 51% increase in property taxes.

That’s the balancing act here.

Yes, cutting charges can help bring on more supply. No, it does not automatically mean every buyer gets a perfectly equal discount.

Whether the end buyer gets the benefit depends on market conditions, financing, land costs, builder margins, and competition at the time. The announcements do not promise that every dollar saved will go straight to buyers. This is where I see an issue and added some BOLD text on builder margins. Is the builder actually going to pass along the savings?

There has been talk about showing consumers what the actual development charges are on each purchase too.

That is interesting!

If buyers start seeing exactly how much of the price is tied to development charges, it could absolutely affect where they choose to buy based on who’s tapped in to the program.

I am certainly in favour of any form of accountability when it comes to government charges and spending.

Where does the $8.8 billion come from?

I think this is a great question to be asking based on a lot of the previous spending.

The announcements say the federal government and Ontario will split the cost. But the public information released so far does not show a neat line-by-line breakdown of exactly which revenue sources or budget lines will fund every dollar.

The money is suppose to come from the Build Communities Strong Fund. This is a $51B fund found somewhere in the federal budget.

Sounds like a mix of tax revenue, reallocated spending, and borrowing. Tax-payer backed government spending and borrowing.

Are they printing money?

Apparently not.

This is not the same thing as a central bank creating money out of thin air.

The immediate mechanism here is government budgeting, taxation, and borrowing. That said, when governments spend heavily while running deficits, that can still affect the economy more broadly. Debt levels matter. Inflation pressure can matter. Financing conditions matter.

But if the question is, “Did they just turn on the money printer for this specific housing announcement?” I’m seeing no. We’ll keep an eye not hat moving forward.

How does the HST rebate actually work?

Most buyers do not get a big, beautiful cheque after closing. In many new-home purchases, the builder handles the rebate paperwork and credits the rebate to the buyer on closing, assuming the buyer qualifies. If they do not qualify, that amount may have to be paid back. The price of the home isn’t reduced to reflect the rebate, it’s credited on the balance sheet at closing.

This is not a brand-new system. It is an expansion of rebate rules that were already in place.

There are two pieces to the tax relief: the Ontario rebate on the provincial part of the HST, and separate federal relief on the federal part. Together, that is why you are seeing numbers as high as $130,000 in potential savings on eligible new homes.

Will buyers definitely save money?

I don’t see it with the development charges. HST yes. And we’ll see housing starts and a flurry of sales thanks to the HST.

The development charge changes are meant to reduce costs. That part is true.

But reducing builder costs does not always mean the sticker price drops by the same amount.

In a slower market, builders may need to pass along more of the savings to move product. In a hotter market why wouldn’t they just take the profits?

The same goes for pre-construction.

Pre-construction pricing is shaped by a lot more than just taxes and fees. Builders are also pricing in financing costs, construction costs, future risk, and where they think the market is headed. So while a rebate can help, it does not automatically make every pre-construction home a great deal.

That said, the expanded HST rebate is meaningful. It is real relief on a product type that has been weighed down by charges for years.

Can they build enough houses to reduce prices?

Supply and demand.

Personally, I still have a hard time seeing how affordability meaningfully improves in major areas like the GTA unless supply dramatically outpaces demand. Can they really out-build demand in the places people want to live most?

If something is priced low, it sells over asking. That’s not going to change in the hot spots.

We did see a version of oversupply hit the condo market. That happened. But could you really see that playing out the same way with detached or town homes in the major areas?

Would lower home prices be good or bad?

Both, depending on how it happens.

More affordable housing is good. That helps people enter the market, move for work, start families, and generally function in the economy.

But a sharp, messy drop in prices can be a problem too. It can hurt homeowners, reduce spending, slow construction activity, and create stress across the market.

Why not just remove the charges and taxes entirely?

Because somebody still has to pay for the infrastructure.

Development charges are not random. Municipalities use them to help pay for the infrastructure needed when communities grow. If cities cut those charges hard, the money has to come from somewhere else or the infrastructure gets shortchanged.

That is why this $8.8 billion plan exists in the first place. The idea is to lower some of the burden on new housing projects while using public funding to soften the hit to municipal finances.

One positive that should not be ignored

Here’s an upside I see that is worth mentioning.

First-time buyers only make up a small slice of the new-home market. It’s about 5 percent. That means the other 95 percent of buyers already own a home and will have one to sell.

That matters because housing activity does not just help one buyer or one seller. Every resale home that sells has a major spin-off effect through the economy. The numbers often cited are around $97,000 in economic spin-off per resale transaction.

New construction has an even larger ripple effect. A new detached home is tied to roughly 3.8 person-years of employment. A condo is about 1.5 person-years. Then you add in appliances, furniture, window coverings, moving costs, renovations, service trades, and everything else that comes after someone takes possession.

So even if someone is skeptical about whether this will solve affordability, there is still a strong argument that more housing activity supports jobs, spending, and economic growth.

In Summary

This is an attempt to make new housing easier to build by covering the cost burden of development charges.

The development charge plan is meant to lower costs on new projects, while public funding helps cover part of what municipalities would otherwise lose.

The HST changes are already in effect and give eligible buyers and rental projects more relief through a rebate system that was already there. They’ve been starving for this.

The idea is to make more projects viable, encourage more building, and move some of the cost away from the point of development and into the broader public system.

Will that actually improve affordability in a meaningful way? Maybe. But that is going to come down to execution, municipal buy-in, market conditions, and whether the savings actually reach the people buying the homes.

Thanks for reading,

Andrew